Taking control of health care expenses is on the top of most people’s to-do list for 2018. The average premium increase for 2018 is 18% for Affordable Care Act (ACA) plans. So, how do you save money on health care when the costs seems to keep increasing faster than wage increases? One way is through health savings accounts.

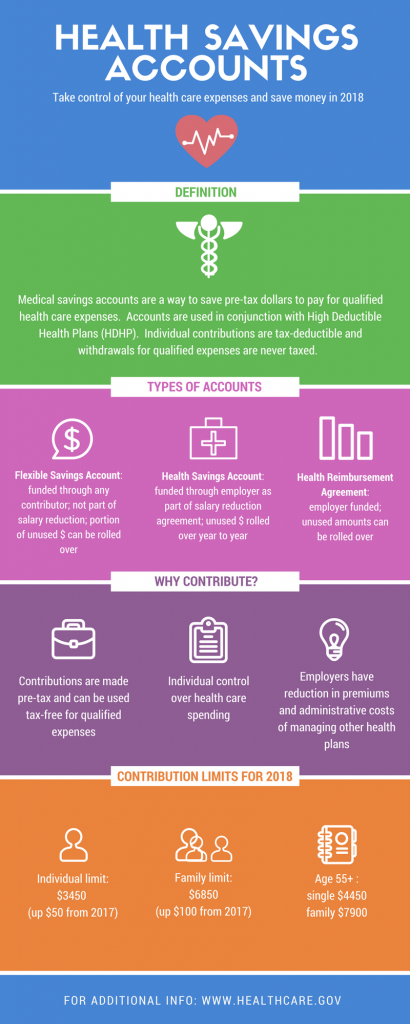

Health savings accounts are used in conjunction with High Deductible Health Plans (HDHP) and allow savers to use their pre-tax dollars to pay for qualified health care expenses. There are three major types of medical savings accounts as defined by the IRS. The Health Savings Account (HSA) is funded through an employer and is usually part of a salary reduction agreement. The employer establishes this account and contributes toward it through payroll deductions. The employee uses the balance to pay for qualified health care costs. Money in HSA is not forfeited at the end of the year if the employee does not use it. The Health Flexible Savings Account (FSA) can be funded by the employer, employee, or any other contributor. These pre-tax dollars are not part of a salary reduction plan and can be used for approved health care expenses. Money in this account can be rolled over by one of two ways: 1) balance used in first 2.5 months of new year or 2) up to $500 rolled over to new year. The third type of savings account is the Health Reimbursement Arrangement (HRA). This account may only be contributed to by the employer and is not included in the employee’s income. The employee then uses these contributions to pay for qualified medical expenses and the unused funds can be rolled over year to year.

There are many benefits to participating in a medical savings account. One major benefit is the control it gives to employee when paying for health care. As we move to a more consumer driven health plan arrangement, the individual can make informed choices on their medical expenses. They can “shop around” to get better pricing on everything from MRIs to prescription drugs. By placing the control of the funds back in the employee’s hands, the employer also sees a cost savings. Reduction in premiums as well as administrative costs are attractive to employers as they look to set up these accounts for their workforce. The ability to set aside funds pre-tax is advantageous to the savings savvy individual. The interest earned on these accounts is also tax-free.

The federal government made adjustments to contribution limits for health savings accounts for 2018. For an individual purchasing single medical coverage, the yearly limit increased $50 from 2017 to a new total $3450. Family contribution limits also increased to $6850 for this year. Those over the age of 55 with single medical plans are now allowed to contribute $4450 and for families with the insurance provider over 55 the new limit is $7900.

Health care consumers can find ways to save money even as the cost of medical care increases. Contributing to health savings accounts benefits both the employee as well as the employer with cost savings on premiums and better informed choices on where to spend those medical dollars. The savings gained on these accounts even end up rewarding the consumer for making healthier lifestyle choices with lower out-of-pocket expenses for medical care. That’s a win-win for the healthy consumer!